Time series Analysis via stochastic volatility models using MCMC methods

Time series analysis is used to estimate and predict behaviour of time dependent processes. In this project we have made use of two stochastic volatility models: Univariate Stochastic Volatility Model, and Multivariate Stochastic Volatility via Wishart Distribution. We estimated their parameters using combinations of MCMC methods, which are mainly Metropolis-Hastings Algorithm and Gibbs sampler. The work done gave us tools to estimate time dependent variance structure of the time series.

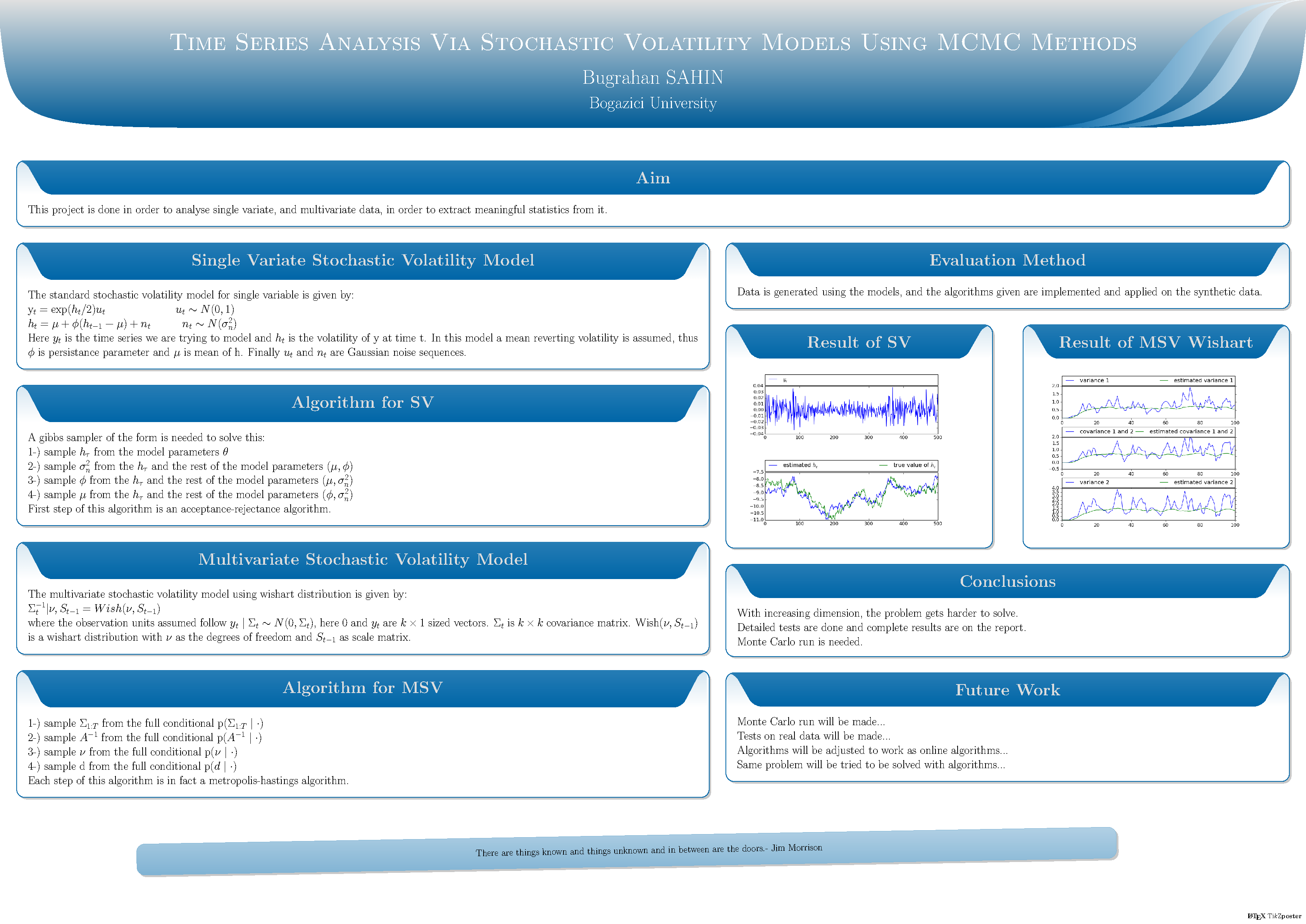

Project Poster:

Project Members:

Buğrahan Şahin

Project Advisor:

Ali Taylan Cemgil

Project Status:

Project Year:

2015

- Fall