Lecture 13 (25 Dec)

Pointers, Call by value, Call by reference, Polymorphism (same name, different functions by arguments)

#include <iostream>

using namespace std;

void fun(int *pa) {

*pa = 3;

}

void fun(int a) {

a = 9;

}

int main() {

int a = 5;

int *p;

p = &a;

cout << a << endl;

// Output: 5

*p = 2;

cout << a << endl;

// Output: 2

fun(&a); // Call by reference

cout << a << endl;

// Output: 3

fun(a); // Call by value

cout << a << endl;

// Output: 3 (not 9)

}

Files, Reading and writing formatted text.

#include <iostream>

#include <fstream>

using namespace std;

// Reads real numbers from an ascii file, omits characters and writes numbers*3 to a new ascii file, one number per line

int main () {

double d; char c;

filebuf fb;

fb.open ("C:\\usr\\cemgil\\tex\\bogazici\\courses\\fe\\myworkspace\\dosyaoku\\test3.txt",ios::in);

istream is(&fb);

ofstream outfile;

outfile.open("C:\\usr\\cemgil\\tex\\bogazici\\courses\\fe\\myworkspace\\dosyaoku\\test4.txt");

while (!is.eof()) {

is >> d; // Read a double

if (is.fail()) { is.clear(); is >> c; cout << c; } // Discard invalid characters

else {

if (!is.eof()) {

cout << d << endl;

outfile << d*3;

outfile.put ('\n');

}

}

};

outfile.close();

return 0;

}

Reference variables, Call by reference.

#include <iostream>

using namespace std;

void fun(int& ar)

{

ar = 2;

}

int main() {

int a = 3;

int b = 7;

int& r = a; // r is an alias of, must be initialised during declaration

r = a;

r = 12;

cout << a << endl;

r = b;

cout << a << endl;

r = 4;

cout << a << endl;

cout << b << endl;

fun(b);

cout << b << endl;

return 0;

}

Lecture 12 (18 Dec)

Lecture 11 (11 Dec)

Lecture 10 (4 Dec)

Lecture 9 (27 Nov)

Lecture 8 (20 Nov)

Lecture 7 (13 Nov)

Lecture 6 (6 Nov)

Option Pricer object

#include <iostream>

#include <cmath>

#include <cstdlib>

#include <algorithm>

#include "nr3_psplot.h"

using namespace std;

// Uniform [0,1] , Warning: cstdlib::rand() is not very reliable

inline double Rand() {return double(rand())/(RAND_MAX+1);};

const double pi = 3.14159265358979323846;

// Box-Muller Transform method, Warning: this implementation is not very efficient

inline double Randn(){return (-2*log(1-Rand())) * cos(2*pi*Rand());};

class OptionPricer {

double r;

double sigma;

double Pricer(double S0, // Current price

double K, // Strike Price

double T, // Expiry time

bool isCall = true

)

{

int MAX_ITER = 1000000;

double ST, CT, W;

double EC = 0;

for (int i=1; i<=MAX_ITER; i++) {

W = sqrt(T)*Randn();

ST = S0*exp((r - sigma*sigma/2)*T + sigma*W);

CT = isCall ? ST-K : K-ST;

if ( CT<0) CT = 0.;

EC = 1./i * CT + double(i-1)/i*EC;

};

return exp(-r*T)*EC;

}

public:

OptionPricer(double InterestRate, double stdVol) {

r = InterestRate;

sigma = stdVol;

};

void Print() {

cout << "InterestRate: " << r << endl;

cout << "Volatility: " << sigma << endl;

return;

}

double CallPrice(double CurrentPrice,

double StrikePrice,

double ExpiryDate)

{

return Pricer(CurrentPrice,

StrikePrice,

ExpiryDate,

true

);

};

double PutPrice(double CurrentPrice,

double StrikePrice,

double ExpiryDate)

{

return Pricer(CurrentPrice,

StrikePrice,

ExpiryDate,

false

);

}

};

int main() {

double S0 = 100;

double K = 100;

double rate = 0.01;

double stdVol = 0.01;

int I = 100;

double dt = 0.1;

OptionPricer o1(0.03, 0.1);

vector <double> t(I);

vector <double> CallPrice(I);

vector <double> PutPrice(I);

o1.Print();

cout << endl;

for (int i=0;i < I; i++) {

t[i] = i*dt;

CallPrice[i] = o1.CallPrice(S0, K, t[i]);

PutPrice[i] = o1.PutPrice(S0, K, t[i]);

cout << i << endl;

};

double maxCall = *max_element(CallPrice.begin(), CallPrice.end());

PSpage pg("plot.ps");

PSplot plot1(pg,100.,500.,100.,300.);

plot1.setlimits(0, *max_element(t.begin(), t.end()), 0, maxCall );

plot1.frame();

plot1.scales(1, dt, maxCall, maxCall/10, 2, 2, 0, 0);

plot1.xlabel("Expiry");

plot1.ylabel("Price");

plot1.lineplot(t, CallPrice);

for (int i=0; i< I; i++) plot1.dot(t[i], CallPrice[i], 5.);

for (int i=0; i< I; i++) plot1.pointsymbol(t[i], PutPrice[i], 109, 5.);

pg.close();

return 0;

}

Option Pricer function

#include <iostream>

#include <cmath>

#include <cstdlib>

using namespace std;

double sigma = 0.1;

double r = 0.1;

double T = 1;

double S0 = 100;

// Uniform [0,1] , Warning: cstdlib::rand() is not very reliable

inline double Rand() {return double(rand())/(RAND_MAX+1);};

const double pi = 3.14159265358979323846;

// Box-Muller Transform method, Warning: this implementation is not very efficient

inline double Randn(){return (-2*log(1-Rand())) * cos(2*pi*Rand());};

double OptionPricer(double S0, // Current price

double K, // Strike Price

double T, // Expiry time

double r, // Interest Rate

double sigma // Volatility

)

{

int MAX_ITER = 10000;

double ST, CT, W;

double EC = 0;

for (int i=1; i<=MAX_ITER; i++) {

W = sqrt(T)*Randn();

ST = S0*exp((r - sigma*sigma/2)*T + sigma*W);

CT = (ST - K);

if ( CT<0) CT = 0.;

EC = 1./i * CT + double(i-1)/i*EC;

};

return exp(-r*T)*EC;

}

int main() {

double sigma = 0.1;

double r = 0.1;

double T = 1;

double S0 = 100;

double K = 100;

double Price;

cout << "S_0 = " << S0 << endl;

cout << "K = " << K << endl;

for (T=1;T<10.;T=T+0.1 ) {

Price = OptionPricer(S0, K, T, r, sigma);

cout << "T = " << T ;

cout << ", Price = " << Price << endl;

};

return 0;

}

Lecture 5 (30 Oct)

Assignment : Vanilla European Option Pricing via Monte Carlo Description .

Generate a plot displaying the price for different strike prices and expiry dates.

A complex number Object

#include <iostream>

#include <cmath>

using namespace std;

class Complex {

public:

double real;

double imag;

Complex(double re = 0., double im = 0.) {

real = re;

imag = im;

};

void Print() {

if (imag>0) {

if (imag==1.)

cout << real << "+" << "j" << endl;

else

cout << real << "+" << imag << "j" << endl;

}

else

if (imag==-1.)

cout << real << "-" << "j" << endl;

else cout << real << "-" << -imag << "j" << endl;

}

double Magnitude() {

return sqrt(real*real + imag*imag);

}

Complex operator+ (Complex c2) {

Complex result(real+c2.real, imag+c2.imag);

return result;

}

Complex operator* (Complex c2) {

Complex result(real*c2.real-imag*c2.imag, imag*c2.real+real*c2.imag);

return result;

}

};

int main() {

Complex c1(1, 1);

Complex c2(3, 7);

Complex c3 = c1 + c2;

Complex c4 = c1*c1;

Complex c5 = c1 + Complex(0, 8.0);

c1.Print();

c2.Print();

c3.Print();

c4.Print();

c5.Print();

cout << c1.Magnitude() << endl;

}

Estimation of pi via Monte Carlo

#include "nr3_psplot.h"

const long int N = 5000; // Number of samples

// Uniform [0,1] , Warning: cstdlib::rand() is not very reliable

inline double Rand() {return double(rand())/RAND_MAX;};

const double pi = 3.14159265358979323846;

// Box-Muller Transform method, Warning: this implementation is not very efficient

inline double Randn(){return (-2*log(Rand())) * cos(2*pi*Rand());};

int main(void) {

PSpage pg("plot.ps");

PSplot plot1(pg,100.,300.,100.,300.);

plot1.setlimits(-1., 1, -1, 1 );

plot1.frame();

plot1.autoscales();

plot1.xlabel("x1");

plot1.ylabel("x2");

int count = 0;

for (int i=1; i<=N; i++) {

double x1 = 2*Rand()-1;

double x2 = 2*Rand()-1;

if (x1*x1 + x2*x2 < 1) {

count ++;

plot1.setcolor(255, 0, 0);

}

else {

plot1.setcolor(0, 0, 255);

}

plot1.dot(x1,x2);

}

cout << "pi = " << double(count)/N*4 << endl;

pg.close();

}

Lecture 4 (23 Oct)

Lecture 3 (16 Oct)

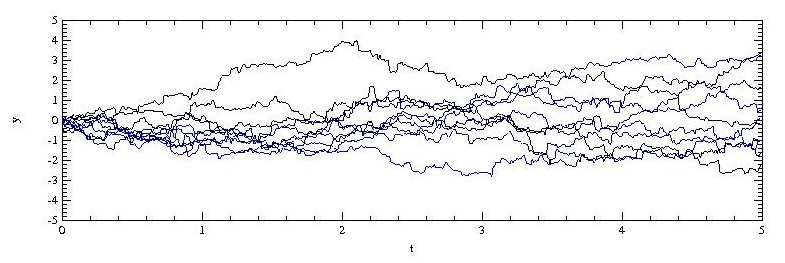

Assignment 1: Generate random walks and plot the moving average. Input the window length from the keyboard.

// Generates a log-return process from a stochastic volatility model

// v[t+1] = a v[t] + epsilon[t]

// epsilon[t] ~ Gaussian(0, sqrt(var dt) )

//

// z[t]|v[t] ~ Gaussian(0, sqrt(v[t+1]))

//

// The output, plot.ps file can be viewed with GSview and ghostscript

// (To download Visit http://pages.cs.wisc.edu/~ghost/ and follow links to GSview)

#include "nr3_psplot.h"

const int N = 200; // Number of steps

const int E = 1; // Number of paths

double T = 5.; // Final time

const double var = 2; // Variance of the random walk

const double a = 1; // AR(1) coefficient

const double dt = T/N; // time increment

// Uniform [0,1] , Warning: cstdlib::rand() is not very reliable

inline double Rand() {return double(rand())/RAND_MAX;};

const double pi = 3.14159265358979323846;

// Box-Muller Transform method, Warning: this implementation is not very efficient

inline double Randn(){return (-2*log(Rand())) * cos(2*pi*Rand());};

int main(void) {

double ep; // Noise, (shock)

vector<double> t(N),v(N); // time index and volatility

vector<double> exp_v(N); // variance

vector<double> z(N); // log returns

vector<double> price(N); // price

PSpage pg("plot.ps");

PSplot plot1(pg,100.,800.,100.,300.);

plot1.setlimits(0., T, -5, 5 );

plot1.frame();

plot1.autoscales();

plot1.xlabel("t");

plot1.ylabel("v");

for (int e=0; e<E; e++) {

v[0] = log(1);

exp_v[0] = exp(v[0]);

z[0] = sqrt(exp_v[0])*Randn();

price[0] = 1;

for (int i=0;i<N;i++) {

t[i] = i*dt;

ep = sqrt(var)*Randn()*dt;

if (i<N-1) {

v[i+1] = a*v[i] + ep;

exp_v[i+1] = exp(v[i+1]);

z[i+1] = sqrt(exp_v[i+1])*Randn();

price[i+1] = exp(z[i+1])*price[i];

}

}

plot1.setcolor(255, 0, 0);

plot1.lineplot(t,exp_v);

plot1.setcolor(0, 0, 0);

plot1.lineplot(t,z);

}

pg.close();

}

#include <iostream>

using namespace std;

int main() {

int N = 9;

int f;

cout << "Carpim Tablosu" << endl;

for (int i=1;i<=N;i++) {

for (int j=1;j<=N;j++) {

f = i*j;

cout << f << " ";

}

cout << endl;

}

return 0;

}

Lecture 2 (9 Oct)

Eclipse: Download the 32 bit version of CDT -- the 64 bit version has some display problems with latest version of MinGW.

Download the header file nr3_psplot.h. This is a slight modification from numerical recipes in C++, V3.

Original documentation of PSPage and PsPlot objects is here.

The output: plot.ps

// Generates discrete time random walks and plots the realisations

// y[t+1] = a y[t] + epsilon[t]

// epsilon[t] ~ Gaussian(0, sqrt(var dt) )

//

// The output, plot.ps file can be viewed with GSview and ghostscript

// (To download Visit http://pages.cs.wisc.edu/~ghost/ and follow links to GSview)

#include "nr3_psplot.h"

const int N = 500; // Number of steps

const int E = 10; // Number of paths

double T = 5.; // Final time

const double var = 25; // Variance of the random walk

const double a = 1; // AR(1) coefficient

const double dt = T/N; // time increment

// Uniform [0,1] , Warning: cstdlib::rand() is not very reliable

inline double Rand() {return double(rand())/RAND_MAX;};

const double pi = 3.14159265358979323846;

// Box-Muller Transform method, Warning: this implementation is not very efficient

inline double Randn(){return (-2*log(Rand())) * cos(2*pi*Rand());};

int main(void) {

double ep; // Noise, (shock)

vector<double> t(N),y(N); // time index and state of the random walk

PSpage pg("plot.ps");

PSplot plot1(pg,100.,800.,100.,300.);

plot1.setlimits(0., T, -5, 5 );

plot1.frame();

plot1.autoscales();

plot1.xlabel("t");

plot1.ylabel("y");

for (int e=0; e<E; e++) {

y[0] = 0;

for (int i=0;i<N;i++) {

t[i] = i*dt;

ep = sqrt(var*dt)*Randn();

if (i<N-1) y[i+1] = a*y[i] + ep;

}

plot1.lineplot(t,y);

int col = int(e/double(E)*255);

plot1.setcolor(0, 0, col);

}

pg.close();

}

Lecture 1 (2 Oct)

Compile the program, produce a.exe

> g++ myprog.cpp

Compile the program, produce myprog.exe

> g++ myprog.cpp -o myprog.exe

Example 3

#include <iostream>

using namespace std;

// Calculate f_{n} = sum_i=1^n i and prints for i=1..n

int main ()

{

int n = 20;

int f;

f = 0;

for (int i=1; i<=n; i++) {

f = f + i;

cout << i << "," << f << endl;

};

};

Example 2

// Prints a table of squares and cubes, waits for input to terminate

#include <iostream>

using namespace std;

int main ()

{

char c;

for (int i=1; i<=10; i++) {

cout << i << " " << i*i << " " << i*i*i << endl;

};

cin >> c;

return 0;

};

Example 1

#include <iostream>

using namespace std;

int square(int x0_input) {

return x0_input*x0_input;

};

int cube(int x0_input) {

return x0_input*x0_input*x0_input;

};

int main ()

{

int i = 0;

double d = 3.14;

char ch = 'a';

cout << "Goodby Moon" << " " << square(5) << " " << cube(5) << endl;

cout << i << endl;

cout << d << endl;

cout << ch << endl;

return 0;

};